Insights

Fed announces largest rate hike in nearly three decades as it seeks to restore price stability

REAL ECONOMY BLOG | June 15, 2022

Authored by RSM US LLP

The Federal Reserve lifted its federal funds policy rate to a range between 1.5% and 1.75% on Wednesday as it moves to restore price stability over the medium term. We now expect the Fed to hike the policy rate by 50 basis points in July and September and then by 25 basis points at each successive meeting.

In our estimation, the first possible opportunity for the Fed to pause in its price stability campaign would be early next year, when the policy rate will rest in a range between 3.25% and 3.5% if the pace and direction of inflation eases in conjunction with central bank policy.

The Federal Open Market Committee did not alter its path of balance sheet reductions, which started this month with $47.5 billion per month and will increase to $95 billion per month starting in September.

The Fed needs to follow through on its forward guidance, which points to a median policy rate of 3.4% by the end of the year. The relative successes of central bank policy in cooling an overheating real economy over the next several months while anchoring inflation expectations will on the margin determine if the economy slips into recession early next year.

Why 75 basis points?

Why did the Federal Reserve lift rates by 75 basis points, which is the single largest move since November 1994, when Alan Greenspan, the Federal Reserve chairman at the time, hiked rates by that same amount? The move was necessitated because of two developments:

- Inflation is broadening out across the economy. Roughly 70% of the consumer price index is now increasing at or above 4% on a year-ago basis, requiring the Fed to act forcefully because it has fallen too far behind the curve.

- The Fed effectively lost control of the inflation narrative. This resulted in a sharp move upward at the front end of the Treasury curve that saw the two-year yield increase by 95 basis points in only 12 trading days between May 30 and June 13 in tandem with the 75 basis-point increase in the 10-year yield over that same timespan. At the start of the year, by contrast, federal funds futures implied a policy rate less than 1%, or where they were just before the policy decision.

More important, those moves inside the Treasury curve along with the increase in near-term inflation expectations represent a loss of credibility and investor confidence. The June policy move represents a major step in the central bank’s attempts to regain that credibility through the restoration of price stability. Credibility and confidence in the central bank will not be restored in the near term and will be measured by how quickly price stability is restored and at what cost to the real economy.

Kansas City Federal Reserve President Esther George dissented in the vote, favoring a 50-basis point move.

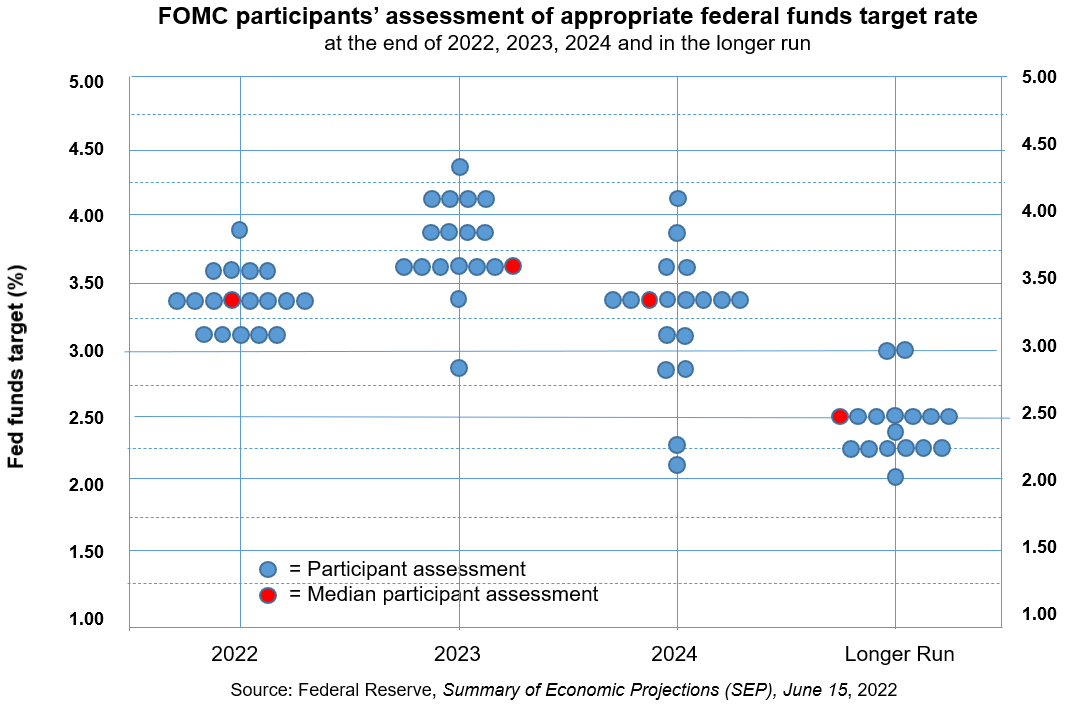

Dot plot

The Fed’s dot plot strongly implies that its benchmark policy rate will reach 3.4% by the end of the year, 3.8% next year and back to 3.4% in 2024. The long-run neutral rate, or the rate at which policy is neither restrictive nor accommodative, remains at 2.5%, which implies that policy will move into restrictive terrain by the fall of this year.

Our conjecture is that the risk around the outlook with respect to a recession should move into the first quarter of next year and thereafter going forward.

Summary of economic projections

The Fed downgraded its growth path through 2024 to below 2%. Real gross domestic product is now expected to expand at 1.7% this year and next, which is just below the 1.8% long-term rate and then at 1.9% in 2024.

The employment outlook was also revised downward, with the unemployment rate now expected to increase to 3.7% by the end of this year, 3.9% next year and 4.1% in 2024.

The most interesting portion of the outlook, and sure to be the one most challenged, is the that headline personal consumption expenditures index is expected to finish the year at 5.2% and the policy-sensitive core variable, the core PCE, is expected to end the year at 4.3%. The top-line aggregate is expected to ease to 2.6% next year and 2.2% in 2024, while the core estimate will ease to 2.7% next year and 2.3% the year after.

To be blunt, this will take not just skill in forecasting the economy but quite a bit of luck with respect to the external sector and an easing of geopolitical tensions that are driving food and energy prices higher.

While the Fed’s statement made a point of reminding the public that the Fed remains strongly committed to returning inflation to its 2% objective, that goal in our estimation is now roughly three years away and that will be if economic conditions break in favor of the Fed’s forecast.

News conference

Federal Reserve Chair Jerome Powell in his prepared testimony kept a 50-basis point hike at the July meeting on the table and did not rule out a 75-basis point increase either, all while being careful to note that the channel through which the Fed acts involves the policy rate that then tightens financial conditions and causes the economy to slow.

He also moved to flesh out what a clear and convincing easing of inflation might look like: inflation flattening out and then a sustained move downward over months. He then chose to pivot toward a comprehensive explanation on why the Fed decided to increase its policy rate by 75 basis points.

The takeaway

The major takeaway from the Federal Reserve’s policy decision is that the benchmark policy rate will increase to a minimum of 3.25% to 3.5% by the end of the year. We do not anticipate any possibility of a pause in the Fed’s price stability campaign until early next year, and that is dependent upon a clear and convincing easing of inflation and an anchoring of inflation expectations. In addition, the downward revision of the growth path, increase in unemployment and inflation remaining elevated imply that the probability of a recession is rising, and we think the first real possibility of the economy falling off a cliff resides in the first quarter of next year.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-06-15.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/fed-announces-largest-rate-hike-in-three-decades-as-it-seeks-to-restore-price-stability/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.