Insights

Inflation has risen - can I really raise my prices?

ARTICLE | March 01, 2022

Authored by RSM US LLP

As companies across industries continue to grapple with inflation at its highest level in 30 years, more executives are taking a closer look at whether to increase prices. But there are more dynamics at play than just rising costs, and businesses need to take a broader view as they assess whether now is the time to make such price hikes.

Rising costs were the second most pressing concern behind labor availability or chief financial officers in the fourth quarter of last year, according to a survey of CFOs conducted by the Federal Reserve Bank of Richmond. CFOs surveyed also believe the elevated costs will last throughout this year. Approximately 90% of firms surveyed reported larger-than-normal cost increases in late 2021 and that figure was up from 80% in the second quarter. Fewer than 20% of CFOs expected costs to decrease in the next six months and most believe they will last 10 months or more into 2023.

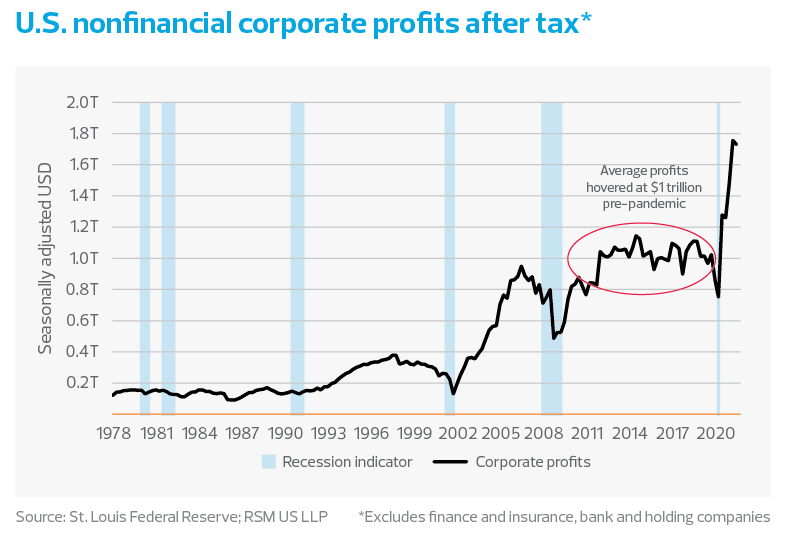

The dour sentiment on cost increases contrasts with the narrative that corporate profits are at their highest level in 70 years. The increase was sudden and swift. In the last decade, U.S. nonfinancial corporate profits after tax hovered around the $1 trillion average annual mark, but by the fourth quarter of 2021, profits rose to $1.7 trillion roughly a 70% increase since the start of the pandemic. This increase suggests businesses benefited from significant pandemic-induced pricing power and have raised prices more than their input costs, fueling more inflation.

Larger firms passed on more of the cost; over 35.3% of large firms surveyed passed on most or all of their cost increases to customers, and 15.3% of small firms reported doing so.

Given that 66% and 70% of large and small firms already report reducing costs in other areas to compensate for increased prices they pay, cost absorption is likely on the horizon for many businesses. This is evidenced by the fact that 50% and 54% of large and small firms, respectively, said they intend to keep prices the same, which means these firms may need to find more ways to cut future costs if prices rise or continue to absorb them.

According to the survey, measures to absorb costs include accepting lower margins, seeking cost reduction, eliminating or substituting product offerings, adding contingency clauses into contracts, and turning down work. Large firms, here again, were less likely to absorb costs with 23.5% reporting having done so versus 35.8% of small firms. This again fits the narrative that the larger the business, the more likely they would pass on costs to the market.

Whether a business can raise prices also depends a lot on its industry. Recent research from the Capital Group looked at businesses with the most pricing power by evaluating gross margin and the standard deviation of those margins over 10 years. Industries with the highest gross margin and the least margin deviation included pharma/biotech, household products, beverages, semiconductors, media, and apparel and luxary goods. Tobacco and software also ranked high but showed the most volatility in margin performance over time.

Industries with somewhat lower but stable margins included groceries, health care services, materials, hardware, telecom, auto and aerospace. Those with higher volatility at the lower end of margin performance included transportation and energy. Making the point on volatility, the latter two are the largest contributors to recent inflationary increases.

Where does this leave middle market businesses?

Does this mean that middle market businesses in some industries should charge ahead with raising prices further? Not necessarily any middle market businesses can raise prices further because of insufficient market share, low product differentiation or competition. But such businesses can still boost their competitiveness in this environment.

Most companies can continue to find low-hanging fruit across their operations. For starters, businesses can assess their pricing behaviors at the business end, where transactions take place with the customer. Performing a series of assessments focused on this area can answer questions about sales efficiency and sales policies, processes for improvement, serving costs of various accounts, and identifying and targeting the most profitable accounts.

Businesses need a unified data set that combines information from their enterprise resource planning, customer relationship management and financial systems. If that data set doesn't exist, then building it is one of the first steps in generating actionable insights.

Analyzing data across these systems will illuminate how efficiently the business model functions. For example, such an analysis can show differences between invoice prices and actual prices paid highlighting possible margin leakage. Additionally, it permits detailed segmentation analysis when slicing data by market, customer, channel or product, which, in turn, can be used to prioritize efforts on the most profitable segments and deemphasize or eliminate those that reduce margin.

Equally important is a qualitative analysis un concurrently with the quantitative analysis that includes structured interviews with key business stakeholders. This taps them for institutional knowledge and will concentrate efforts on where in the data to look for opportunities.

An important area to examine should include the sales processes, which should be documented from end-to-end using interviews as input. It also critical to probe sales team compensation structures to understand current behavior incentivization. For example, are sales teams being compensated on sales volume or margins?

Completing these initial assessments can uncover quick, low-effort wins that if executed properly could result in a 1% to 3% lift in bottom line performance within 12 months. Initial, longer-term projects identified can be quantified from the level of effort, costs and potential payback.

This initial assessment will not reveal an exhaustive list of actions businesses can take. Rather, it lays the foundation for additional projects the business can investigate, such as customer demand modeling, competitive assessments, firsthand intelligence gathering on customers through interviews, detailed analysis on policies, effective tax rate analysis and technology assessments. The key is to find insights that permit decision-makers to prioritize efforts through understanding the costs to implement solutions and determine the expected payback. These insights provide management with a cost-benefit analysis that can help prioritize future projects and maximize return on investment.

The way forward

Inflationary input cost increases aren't permanent, but they will likely persist throughout this year and force additional increases in costs, prices and cost cutting. Middle market businesses that lack additional pricing power will be incentivized to find other ways to cut costs versus absorbing them in the future. Finding these areas of opportunity builds resiliency whenever margins are under pressure.

Companies need to look closely at the transaction level data in detail to understand pricing behaviors across their organization. Building a unified data set and reviewing policies at the customer transaction level will yield additional savings and are worth the effort. The reward for getting pricing behavior and profitability improvements right is one of the most powerful profit levers a company has, and it can become a competitive advantage that middle market businesses can sharpen over time.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Matt Dollard and originally appeared on Mar 01, 2022.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/economics/inflation-has-risen-can-i-really-raise-my-prices.html

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.