Insights

Puerto Rico issues guidance for transfer pricing compliance

ARTICLE | September 21, 2021

Authored by RSM US LLP

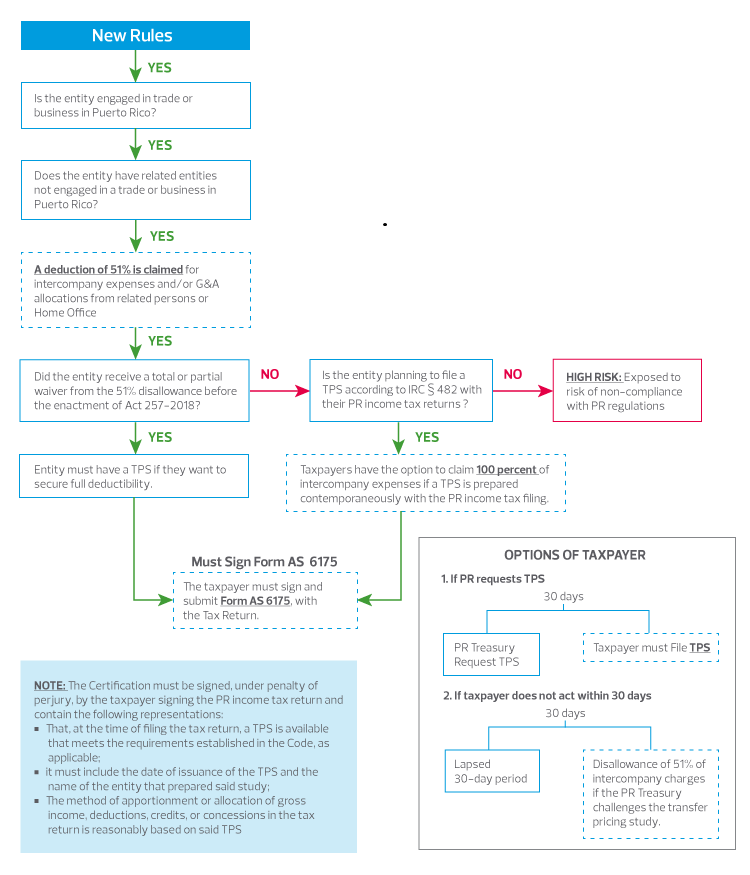

On May 11, 2021, the Puerto Rico Treasury Department (PR Treasury) issued Administrative Determination No. 21-05 (DA 21-05), establishing new rules that would require a transfer pricing study (TPS) to deduct cross-border expenses incurred with related entities not engaged in trade or business in Puerto Rico.

This article will discuss section 1033.17(a)(17) of the 2011 Puerto Rico Internal Revenue Code (the Code) and DA 21-05, which provides guidance for filing a TPS with the PR Treasury and clarifies new compliance requirements where there are transactions between affiliated entities in PR and the US. In addition, the article will briefly highlight Administrative Determination No. 21-08 (DA 21-08), which clarifies that the 30-day filing requirement applies to the TPS and not Form AS 6175 as required in DA 21-05.

Background

Puerto Rico has historically maintained a hands-off approach providing little to no guidance on transfer pricing. In recent years, new non-transfer pricing provisions have been introduced into the Puerto Rico tax rules, some of which affect intra-group transactions.

Act 257-2018 modified the 51% limitation allowing taxpayers to deduct 100% of expenses paid to related parties that operate within Puerto Rico and have related entities not engaged in a trade or business in Puerto Rico.

For tax years beginning after Dec. 31, 2018, the new rules allow such expenses to be fully deductible, provided the taxpayer:

- Signs and submits the approved Form AS 6175 Certification of Compliance (Certification) under penalty of perjury with the tax return.

- Prepares a TPS to confirm that the transaction(s) are arm's length based on sections 482, 6662, and associated regulations; and

- Completes the TPS contemporaneously with the tax return filing that reflects such transfer prices.

- Only reports submitted in accordance with US regulations will be accepted.

For the impact of changes to transfer pricing guidance under PR IRC, see below:

New disallowance limitation (section 1033.17(a)(17))

Transfer Pricing Study (TPS) under section 482

In preparing a contemporaneous transfer pricing study, a taxpayer must use the latest available information and data to establish its transfer pricing policy. The purpose of a taxpayer's TPS is to confirm that its transactions with related parties are priced consistently with the arm's length standard.

The following table presents a summary of TPS requirements under section 482:

| Scope | TPS requirements |

| Who must prepare? | Taxpayers who meet either of the following conditions: Taxpayers with controlled transactions are required to maintain TPS, as covered in section 6662, to avoid penalties in the event of an audit or adjustment to taxable income. Taxpayers planning to claim an exemption from the 51% disallowance on intercompany transactions. |

| What to prepare? | Information as prescribed in section 482 (Transfer Pricing Documentation) Rules that covers: An overview of operations relevant to the business operations in Puerto Rico and; The taxpayer's business and the transactions with its related parties, including functional analysis and transfer pricing analysis |

| When to complete TPS documentation? | By the filing due date of the tax return: |

| What is the penalty for failing to file the TPS? | There are no explicit penalties for failing to comply with the local transfer pricing guidelines. However, in an audit contesting the TPS, the PR Treasury would disallow the 51% deduction of intercompany expenses. |

| Benefit of a TPS? | Taxpayers subject to the limitation explained above have the option to claim 100% of intercompany expenses if a TPS is prepared with the PR income tax filing. |

Takeaway

While taxpayers are not required to submit a TPS with the tax return, preparing a transfer study allows taxpayers to claim 100% of the deductions on intercompany expenses.

With the transfer pricing guidelines now firmly established, and an increased focus on audit activity, taxpayers should verify that their processes and documentation are up to date and compliant with these new requirements. PR Treasury has provided clear and extensive administrative guidance to inform taxpayers and assist them in complying with transfer pricing obligations. This guidance will continue to evolve as practical and technical issues arise in practice.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Ramon Camacho and originally appeared on Sep 21, 2021.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/tax-alerts/2021/puerto-rico-issues-guidance-for-transfer-pricing-compliance.html

The information contained herein is general in nature and based on authorities that are subject to change. RSM US LLP guarantees neither the accuracy nor completeness of any information and is not responsible for any errors or omissions, or for results obtained by others as a result of reliance upon such information. RSM US LLP assumes no obligation to inform the reader of any changes in tax laws or other factors that could affect information contained herein. This publication does not, and is not intended to, provide legal, tax or accounting advice, and readers should consult their tax advisors concerning the application of tax laws to their particular situations. This analysis is not tax advice and is not intended or written to be used, and cannot be used, for purposes of avoiding tax penalties that may be imposed on any taxpayer.

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.