Insights

RSM US Manufacturing Outlook Index: Decelerating growth as tensions mount

REAL ECONOMY BLOG | April 29, 2022

Authored by RSM US LLP

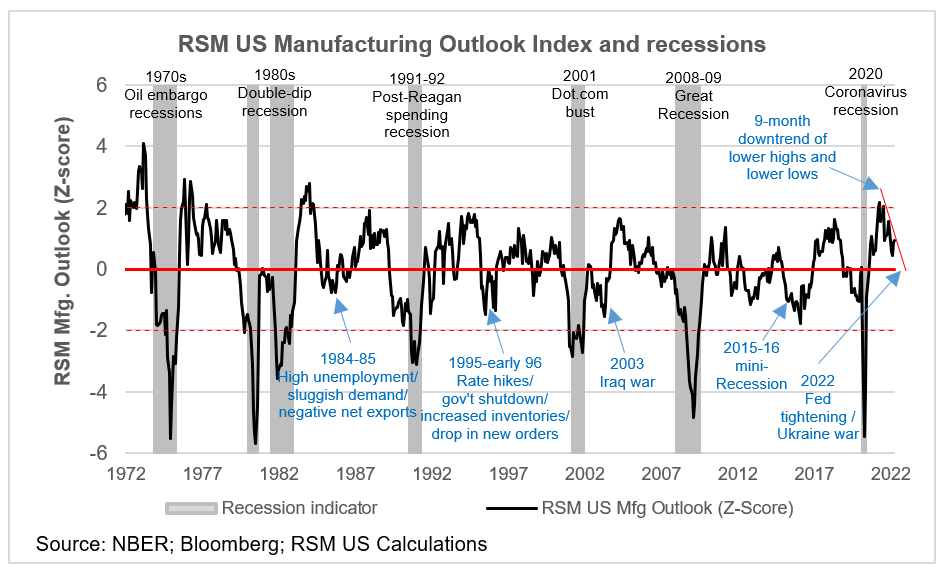

The deceleration of manufacturing is now in its ninth month, with the RSM US Manufacturing Outlook Index signaling the potential for further economic moderation from rising prices and slowing demand.

Geopolitical uncertainty and a resurgent coronavirus in China could bring additional caution in the investment decision process.

A deeper dive into the RSM survey suggests that geopolitical uncertainty and a resurgent coronavirus in China could bring additional caution in the investment decision process.

While business investment remains robust, business sentiment has taken a hit as oil and commodity prices surged this winter and businesses moved cautiously in an uncertain pricing environment. We continue to make the case that this moderation will most likely resemble past midcycle slowdowns and not an outright recession in the near term.

As our analysis indicates, the RSM index rarely goes above 2.0 standard deviations, with most of these brief elevated episodes immediately following a recession.

Although this month’s index value of 0.9 standard deviations remains comfortably above normal manufacturing conditions, the jagged downtrend since last year’s peak mimics the midcycle downturns that have occurred in recent business cycles.

If the trend continues, this episode might best resemble the 1995-96 downturn when the economy slowed as the Federal Reserve hiked rates on inflation fears. The result was a large inventory overhang and a drop in new manufacturing orders.

In the past few months, just as it seemed logistics bottlenecks might begin to unwind, the global economy has been hit by a new series of crises. There is an impending energy crisis in Europe, a resurgence of the pandemic in China and the prospect of more product shortages.

The across-the-board increases in prices are likely to prompt a quick response by the monetary authorities among developed economies, resulting in slower economic activity.

Regional Federal Reserve surveys

There continue to be noticeable month-to-month differences in manufacturing conditions among the regional Federal Reserve surveys.

Notably, activity in New York was up considerably at the beginning of April; activity in the Philadelphia, Dallas and Kansas City regions moderated; and activity in the Richmond region held steady. One constant, however, was the across-the-board decrease in expectations for activity over the next six months.

Business activity in New York State rebounded after falling in March to its lowest level since May 2020. In the survey conducted in the first week of April, 40% of respondents reported that conditions had improved over the month, while 15% reported that conditions had worsened.

New orders and shipments increased dramatically compared to March, while prices remained high.

These gains, though, were accompanied by a downturn in expectations for activity over the next six months. Interestingly, expectations for technology spending turned up again.

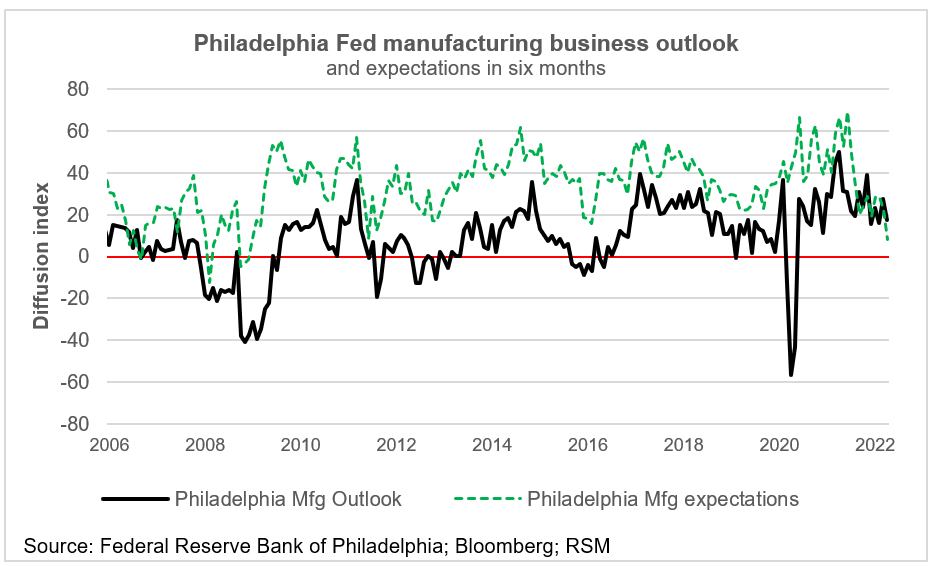

The Federal Reserve Bank of Philadelphia, in its survey conducted during the second week of April. reported a deceleration in the expansion of manufacturing activity. Indicators for current general activity, shipments and new orders declined from last month’s readings but remained positive. The employment index and prices edged higher from already elevated levels.

Indicators for future activity and new orders plunged. Although firms continue to expect growth over the next six months, this is the first time since the mortgage crisis and the pandemic that the expectations index has fallen below the current activity index.

In special questions on labor costs, 80% of the firms indicated that wages and compensation costs had increased over the past three months, 20% reported no change, and none reported decreases. Sixty-five percent of respondents reported plans to increase wages and compensation by more than originally planned.

In special questions on production costs, median expectations for price increases this year were: oil (7.5% to 10%), other raw materials (10% to 12.5%), intermediate goods (7.5% to 10%), and wages and benefits (5% to 7,5%).

Factory activity in Texas continued to expand, but at a more moderate pace in April, according to the Dallas Fed survey conducted April 12 to April 20.

The new orders index inched up and maintained its growth rate. Capacity utilization was unchanged, and the shipments index pushed higher.

Factory activity in Texas continued to expand, but at a more moderate pace in April.

The employment component held its highly elevated reading, with 34% of firms noting net hiring and 10% noting net layoffs. Hours worked slipped.

Prices and wages continued to increase strongly in April, though they eased off their historical highs. The raw materials prices index fell to its lowest reading in more than a year. The wages and benefits index was down slightly from its high of last month but is still markedly elevated.

Expectations regarding future manufacturing activity generally eased but remained positive.

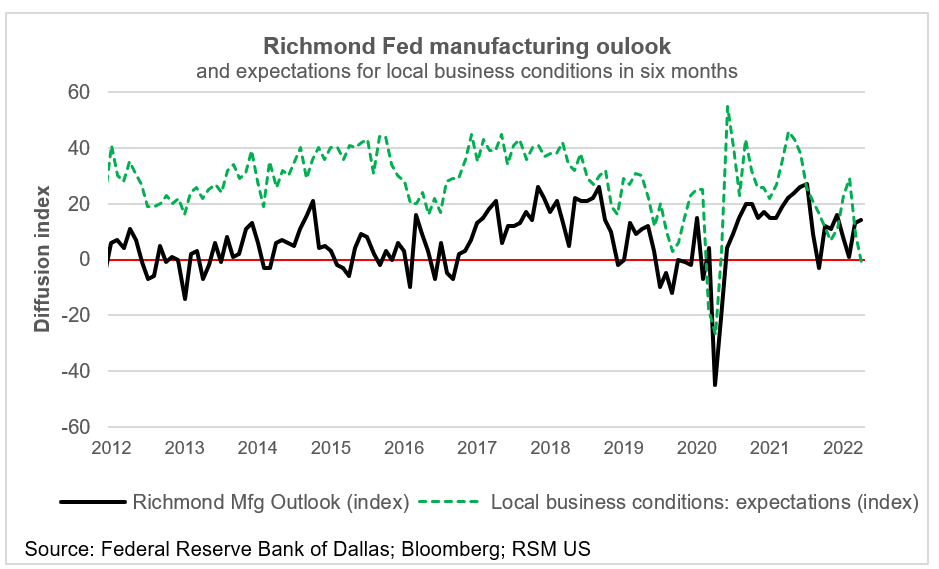

Although manufacturing in the Richmond Fed’s Fifth District remains expansionary, firms were nevertheless pessimistic about current business conditions, according to a survey released on April 26. As such, the composite index of manufacturing activity in the Southeast continues to decelerate, with firms anticipating further deterioration in the next six months.

Responses to a question concerning expectations for local business conditions turned negative for only the third time, with the other two occurring at the start of the pandemic.

Firms reported increases in shipments in April, while the volume of new orders moved down slightly. Though manufacturers continued to report growth in employment, they continued to experience difficulty finding workers with the necessary skills.

Firms do not expect increases in wages to let up, and prices paid for raw materials increased slightly again in April but are expected to decrease somewhat in the next 12 months.

Manufacturing activity in the Kansas City Fed’s Tenth District moderated in its report released on April 28. Increased growth was reported in the production of computer and electronic products, primary metals and furniture. Declines were reported in transportation equipment, electrical equipment, appliances and food manufacturing.

Expectations for manufacturing activity in six months decreased slightly during April, with responses for future shipments, new orders and employment all inching lower. Expectations for the capital expenditures index were unchanged, however.

The reaction to COVID-induced lockdown in China was that 70% of firms reported higher supply chain disruptions and 57% reported higher input prices. A significant share of firms reported no change in demand, capital spending, hiring and inventories, although 17% of firms reported lower inventories.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-04-29.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/rsm-us-manufacturing-outlook-index-decelerating-growth-as-tensions-mount/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.