Insights

We are proud to be named a West Coast Regional Leader for 2024

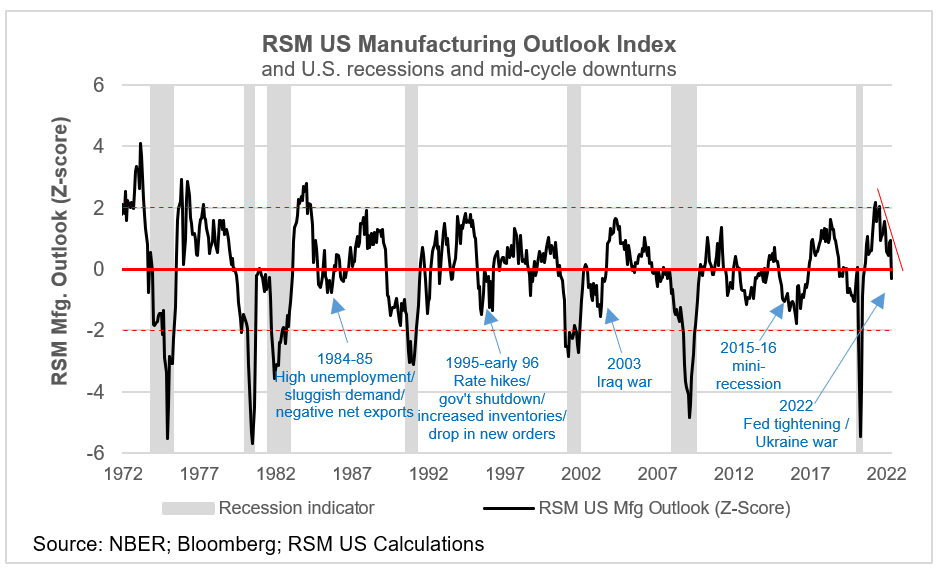

RSM US Manufacturing Outlook Index shows 35% probability of recession over next year

REAL ECONOMY BLOG | May 31, 2022

Authored by RSM US LLP

The RSM US Manufacturing Outlook Index declined into negative terrain in May, signaling the impact of high inflation, rising interest rates, the lockdowns in China and the war in Ukraine.

Circumstances beyond the normal ebb and flow of the business cycle are taking a toll on manufacturing.

While this decline does not imply that the manufacturing sector or the U.S. economy has fallen into a recession, it does support our estimation of a 35% probability of an economic contraction over the next 12 months.

This month’s negative reading of 0.3 standard deviations below normal for manufacturing conditions is a concern in its own right.

But coming in the wake of the Federal Reserve’s actions to slow an overheating economy—and confront the shocks of the war in Ukraine—it appears that circumstances beyond the normal ebb and flow of the business cycle are taking a toll on manufacturing.

Whether this downturn spreads to the rest of the economy will depend on external events and how forcefully the Fed acts to squash inflation.

As the Federal Reserve raises interest rates, those increases will have a direct impact, though with a lag, on the financial sector, housing, autos and broader manufacturing ecosystems.

Given that the Fed is six months into its rate hike cycle, we have arrived at the point where activity in the real economy should slow.

The index

Our index is a composite of surveys of current manufacturing activity conducted by five regional Federal Reserve banks. And because of the knock-on effects to the downstream economy, the health and prospects of the manufacturing sector are indicative of potential economic growth.

The RSM US Manufacturing Outlook Index rarely goes above or below 2.0 standard deviations from normal, with zero defined as normal. Most of these brief elevated episodes occur when the economy first comes out of a recession or after the periodic mid-cycle disruptions to economic recoveries.

Most of the sharp downturns in the manufacturing index—like those we are seeing this month—were prompted by drastic changes in fiscal or monetary policy or by events like the war in Ukraine that can send a shock wave through the economy.

The uneven impact of economic shocks

There can be positive shocks and negative shocks that will affect the rate of economic growth.

The most recent positive example was the sudden increase in consumer demand for products and construction during and then after the pandemic shutdown.

Income assistance and increased demand turned out to be the catalyst for the resurgence of manufacturing, while low interest rates formed the basis for increased investment in productivity.

In terms of negative shocks, the inability to quickly restart some industries after the pandemic shutdown and the inadequacies of the domestic supply chain have created inflationary pressures for both consumers and producers.

The Fed’s tightening of monetary policy in response to inflation will most likely result in reduced demand for products and slower economic growth.

The latest regional bank surveys are pointing to the sum of these disruptions leading to diminished activity in the manufacturing sector.

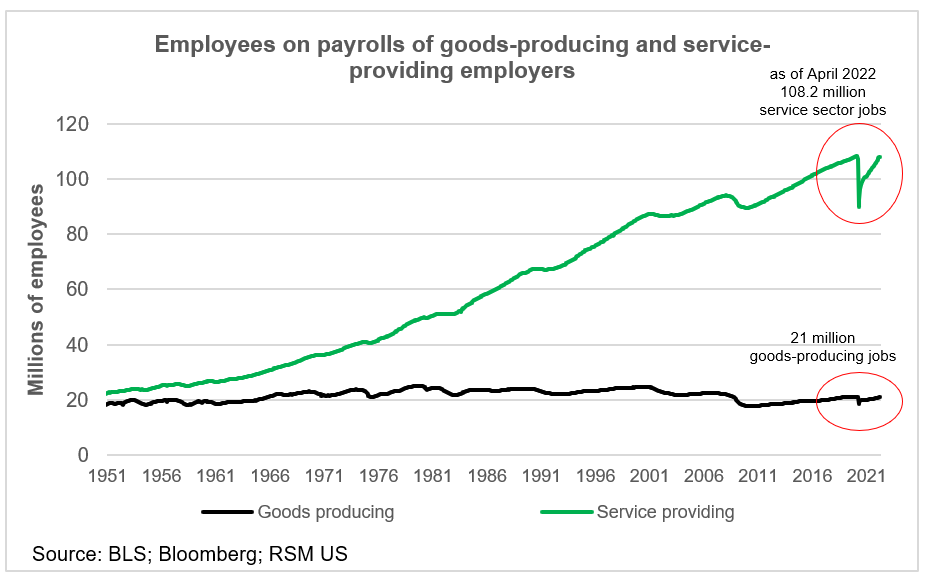

Will this lead to an outright recession? The impact of a manufacturing slowdown in an economy dominated by the service sector is likely to be uneven.

Just as the tariffs of 2018 led to the global manufacturing recession of 2019-21 but not a full-blown recession in the overall economy, not every sector will be affected if growth in the manufacturing sector takes a pause, and not every occupation will immediately incur higher rates of unemployment.

To begin with, for every job in the U.S. goods-producing sector, there are more than five times the number in the service sector.

And the manufacturing sector continues to undergo changes in its demand for labor, adopting technological advancements to compete with the rest of the world.

Within the manufacturing surveys, firms reported shortages of qualified workers, while simultaneously dealing with workers’ expectations of increased employment and wage gains

Along with employers trying to hold onto employees, that suggests a lower likelihood of immediate layoffs should a full-blown manufacturing slump continue.

In addition, surveys since the recovery from the pandemic began indicate manufacturers are increasing their capital investment, suggesting efforts to increase productivity and reduce demand for non-essential labor, all of which can support higher wages

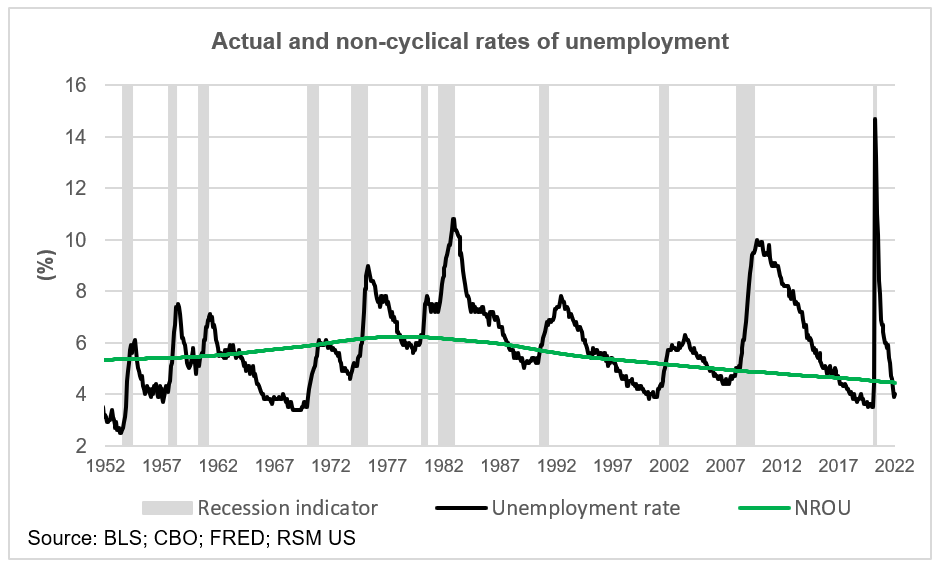

Finally, the current 3.6% rate of unemployment is below the 4.4% estimate of the normal level of labor market churn as employees move from job to job. (In normal times, this would have given room for the Fed to gradually increase interest rates even as it redefined its mandate for full employment to include equal access to employment.)

So because of tightness in the labor market and unless economic conditions in Ukraine and the European Union take a dramatic turn for the worse, we don’t expect the U.S. unemployment rate to increase overnight as it tends to do during an outright recession.

In fact, the Congressional Budget Office is anticipating expansion in the labor market, increased spending on services, and real gross domestic product growth of 3.1% this year. By next year, the CBO expects that the tightening monetary policy and waning fiscal support will have resulted in 1.6% growth of total output.

Still, the negative reports from manufacturers in two of the five Federal Reserve regions and the signs of worsening demand in the other three regions are a warning for the monetary authorities to pursue prudent measures to restrain inflation and for the fiscal authorities to prepare for loss of income should the impact of the war spread.

As in previous business cycles, an economic recovery will begin to moderate at some point but will not fall into a recession until a shock pushes it over the edge.

Regional results

In a reversal from last month, manufacturing activity in New York State dropped sharply. In the survey conducted between May 2 and May 9, new orders declined and shipments fell at the fastest pace since early in the pandemic. In addition, firms were less optimistic about the six-month outlook than at the start of the year. The capital expenditures index fell to its lowest level in several months.

Still, there were modest improvements in employment, a contradiction which in our opinion reflects the difficulty of retaining employees.

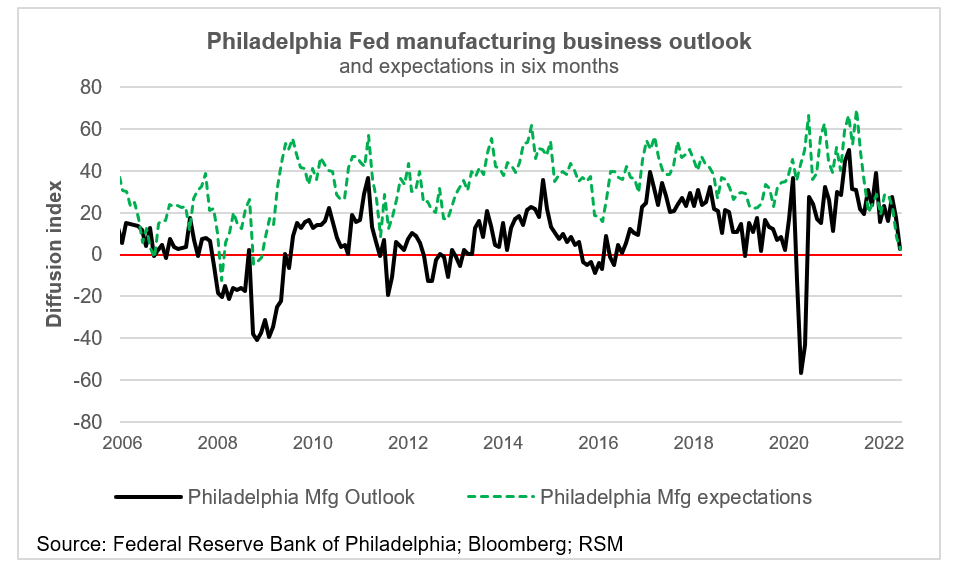

There were mixed results in the survey of manufacturers in the Federal Reserve Bank of Philadelphia’s region collected during the week of May 9 to May 16. While more than half of the firms reported no change from last month, only 22% of the firms reported increased activity versus the 20% that reported a decrease. And while new orders and shipments rose during the month, expectations for employment decreased.

Finally, although firms continue to expect growth over the next six months, the diffusion index for future general activity posted its lowest reading in more than 13 years and the future capital expenditures index fell to its lowest reading since February 2016.

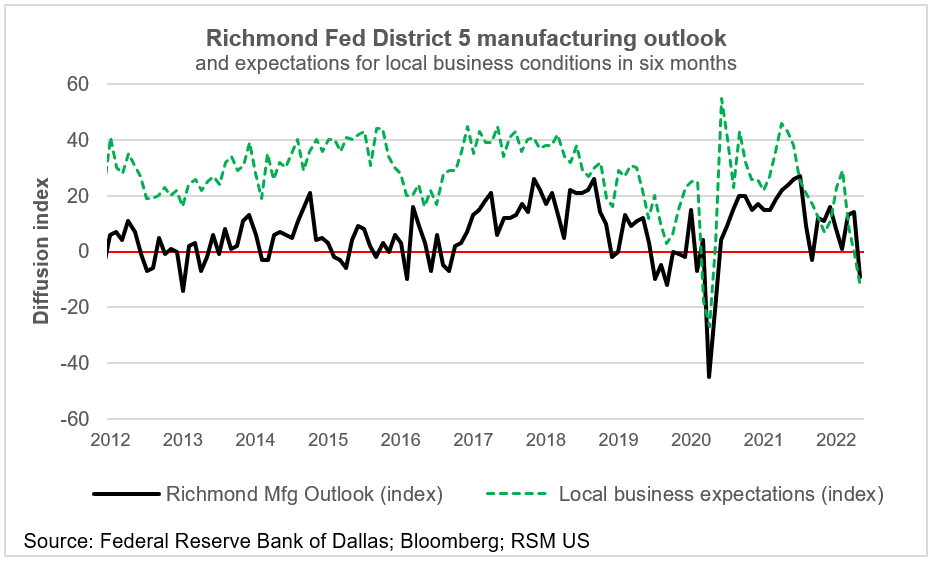

The index of manufacturing activity in the Richmond Fed’s Fifth District turned negative for the first time in eight months, with declines in shipments and new orders. The employment component of the composite index fell substantially from April but was sticky enough to remain positive in a region finding difficulty in staffing qualified employees. Firms continued to report increasing wages.

The May 24 report also found that local business conditions in the Southeast declined further, illustrating the service sector’s dependency on the health of manufacturing. Also, firms have become less optimistic about conditions in the next six months, with diminished expectations for capital spending.

On a bright note, supply chain issues appear to be lightening up with vendor lead times subsiding.

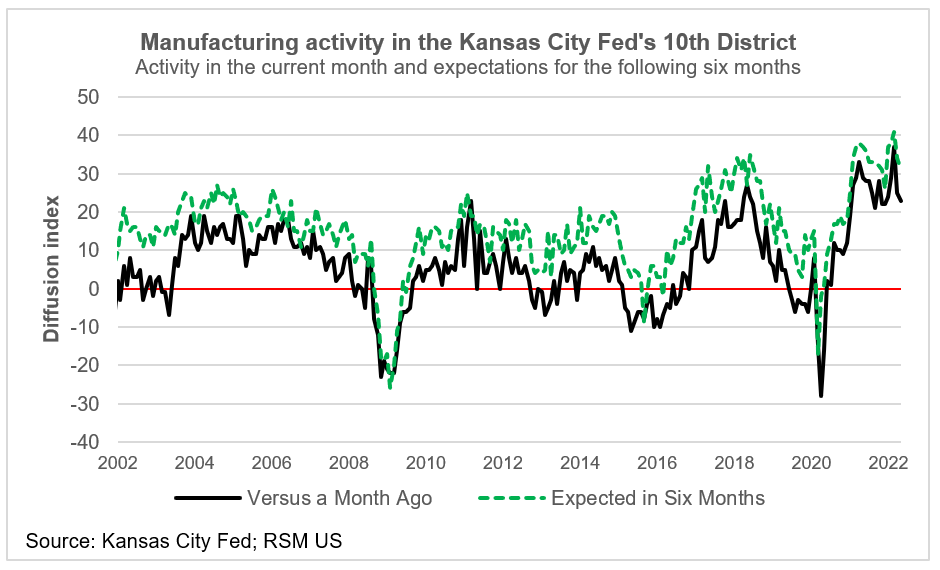

Manufacturing activity continued to expand in the Kansas City Fed’s Tenth District but at a slower pace than its two-decade peak in March. Durable goods plants were the drivers of growth, especially transportation equipment, electrical equipment and furniture-related product manufacturing, according to the report released on May 26. Expectations for manufacturing activity in six months’ time peaked in March as well.

Comments from respondents point to the lack of qualified labor and to supply chain issues, rising prices and increased consumer austerity, all of which in our opinion could constrain further expansion.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-05-31.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/rsm-us-manufacturing-outlook-index-shows-35-probability-of-a-recession-over-next-year/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.