Insights

We are proud to be named a West Coast Regional Leader for 2024

The dollar's reign will continue amid a global flight to safety

REAL ECONOMY BLOG | September 14, 2022

Authored by RSM US LLP

The U.S. dollar is on a tear, increasing in value against its traditional trading partners as well as against the Chinese renminbi.

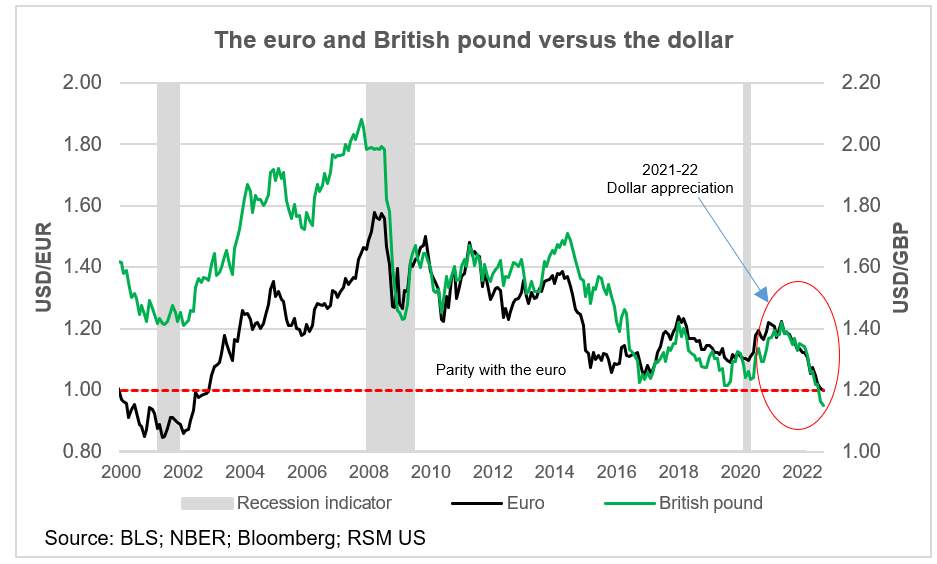

Since Jan. 1, the dollar has appreciated by roughly 12% versus the euro, 15% against the pound and 25% against the yen.

A combination of factors is fueling the surge, including rising interest rate differentials, a global move to the safe haven of the dollar and an escalation of geopolitical tensions, especially in Ukraine.

The economic implications are straightforward. A stronger dollar tends to dampen inflationary pressure as Americans gain greater purchasing power. In a time of rising inflation, this is not insignificant. As the dollar rises, the price of imports falls, which in turn lowers costs for consumers and businesses.

At the same time, though, the cost of exports increases, which reduces profit margins for multinational companies that ship their goods abroad.

The result has been a stunning rise in the dollar’s value. Since Jan. 1, the dollar has appreciated by roughly 12% versus the euro, 15% against the British pound, and 25% against the Japanese yen.

Overall, the U.S. dollar index has surged by 15% this year, with a more than 4% increase over the past 30 days alone as the impact of the war in Ukraine and the European energy crisis has set in.

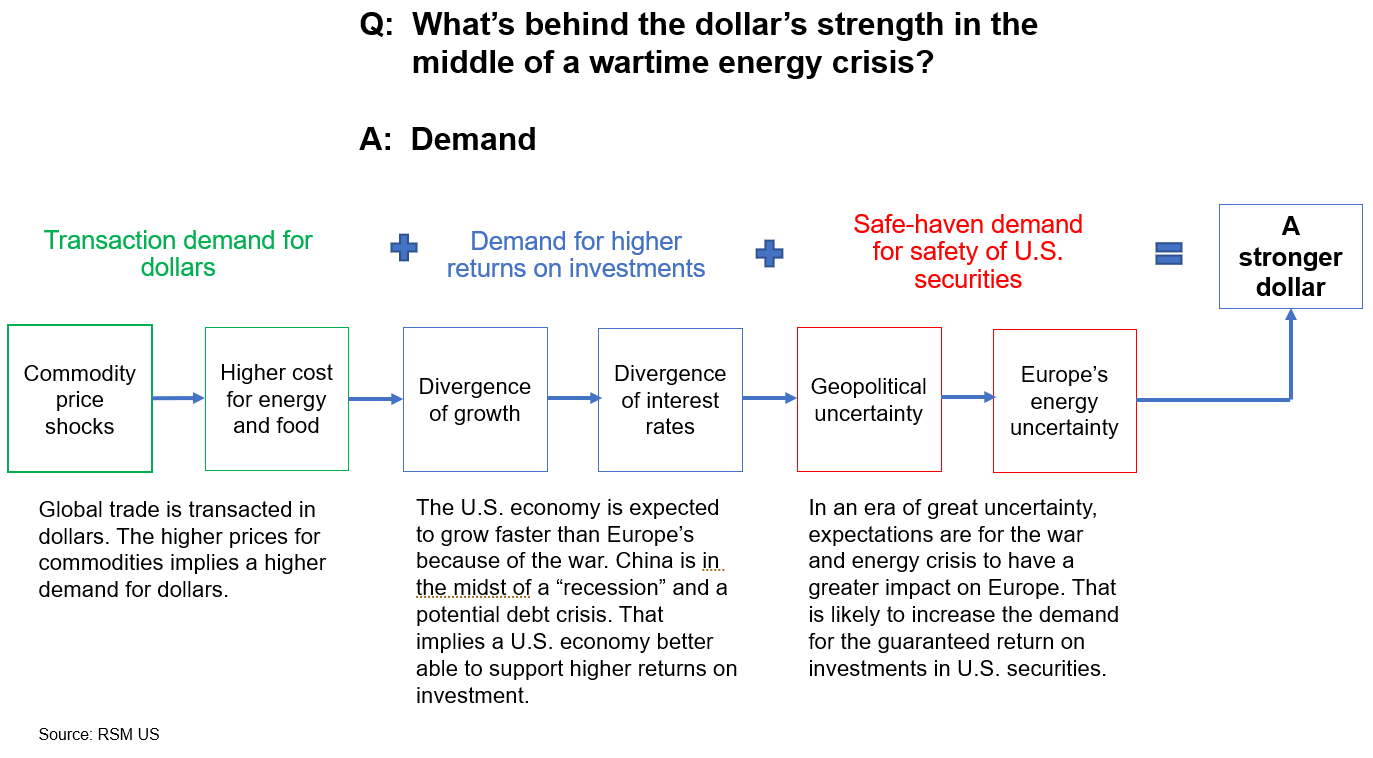

What’s behind the dollar’s surge?

Even with the recent runup, all signs point to continued dollar strength.

The Federal Reserve is poised to hike its policy rate by 75 basis points this month, which will further increase demand for Treasury securities. And the looming price cap on Russian oil, to be imposed on Dec. 5, will help push foreign exchange markets toward one of the bigger moves to the dollar in recent memory.

To better understand what is behind the dollar’s rise, consider three factors:

Transaction demand: Global trade is transacted in dollars, for many good reasons including access to credit and the reliability of billing.

In 2020, the Bank for International Settlements reported that although the United States accounts for a quarter of global economic activity, half of all cross-border bank loans and international debt securities are denominated in U.S. dollars.

Now, limited supplies of food and energy are leading to higher costs, and these transactions are priced in dollars, which only increases the demand for dollars.

The search for higher returns: Within the global search for yield, particularly in a world dominated by real negative interest rates, international investors will look for securities that offer both a nominal return on investment and a currency return.

The demand for dollar-based investments will be determined by the positive divergence in expectations for U.S. economic growth versus its trading partners and by the divergence in interest rates as monetary policy responds to that growth.

The difference in potential economic growth appears to be a byproduct of the energy crisis in Europe. While the consensus expects U.S. real gross domestic product growth to slow to 1.6% this year, and then to 0.9% next year, the odds suggest that Germany’s growth will slow to 1.5% this year, followed by 0.4% next year.

That forecast for next year is almost certainly optimistic given the likely recession at the EU doorstep that will generate a divergence in monetary policy between Europe and the United States.

In the United States, by contrast, expectations are that the more robust U.S. economy will support higher short- and long-term interest rates than those in Europe.

This divergence is reflected in forecasts for the Federal Reserve and European Central Bank. While the Federal Reserve is expected to raise its policy rate to 3.75% by the end of this year (we have forecast 4% or greater), the European Central Bank is expected to raise its policy rate to only 1.5%.

In terms of the return on long-term investments, 10-year U.S. Treasury bonds are yielding about 3.2% augmented by a strengthening dollar.

German 10-year bonds are expected to return only 1.4% this year and next, which offers little cushion to international investors if the euro were to weaken compared to the dollar.

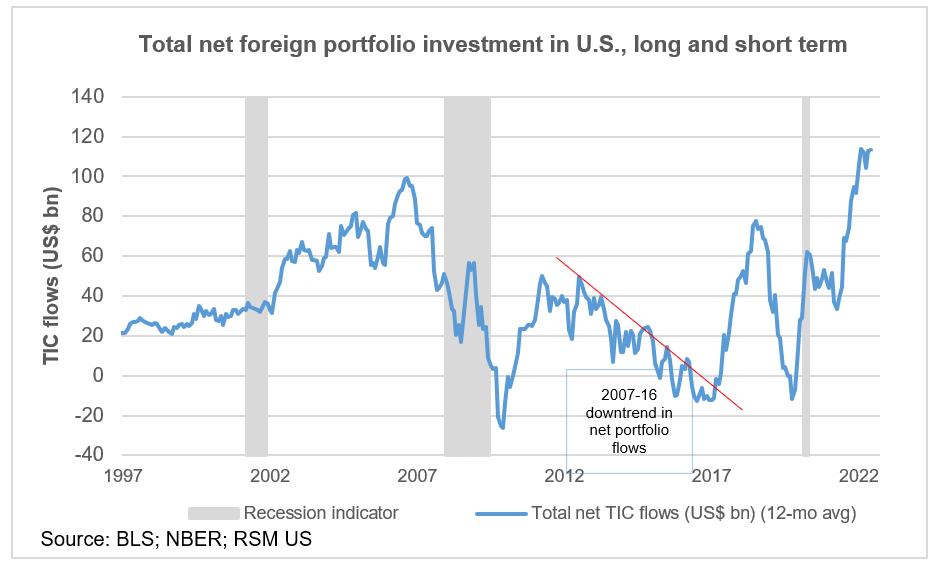

Safe-haven demand: Amid the global turmoil, a flight to the safety of U.S. assets is taking place. Just as U.S. investors will forgo investment in higher-risk corporate bonds during periods of economic distress, international investors will seek the safety of the guaranteed return of U.S. government securities.

The alternative is to risk the impact of further geopolitical uncertainty and limited energy supplies on their individual economies.

China and currency manipulation

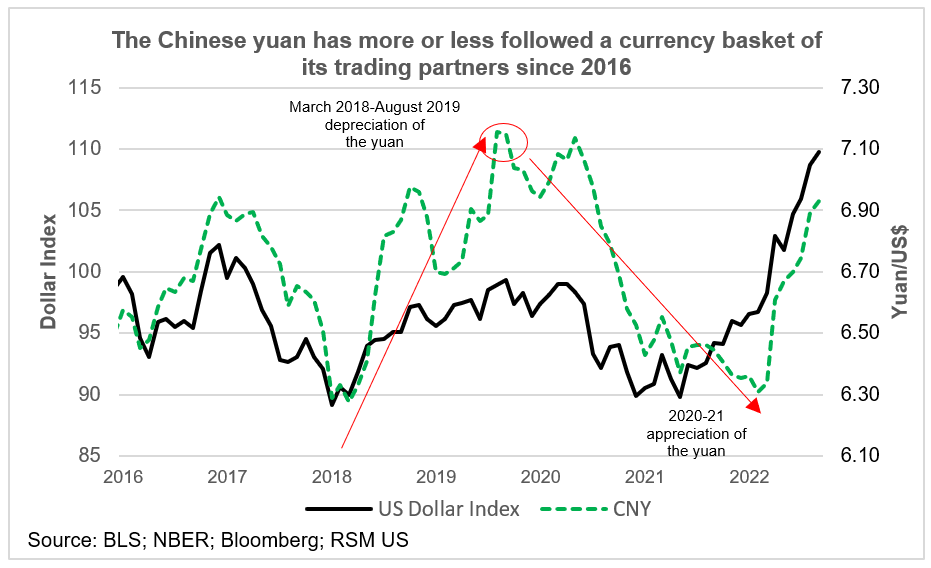

Then there is China. The dollar has increased by roughly 9% versus China’s yuan since the end of last year, a rise that in the past would have prompted outcry from the United States. But times have changed, and so far the reaction to that increase from American officials has been benign.

With China’s growth easing, it would not be any surprise if authorities tolerate a wider band in the yuan’s value.

With China’s growth easing toward 2% and its continued use of economic restrictions to fight COVID-19 outbreaks, it would not be any surprise if Chinese authorities tolerate a wider band in the yuan’s value and the currency depreciates further in the near term.

That stands in contrast to 2019, when the U.S. administration accused China of devaluing its currency despite the across-the-board increase in the dollar’s value versus the rest of the world.

China had abandoned its overt mercantilist pegging of the yuan in 2005, apparently opting for a loose peg against a basket of their trading partners’ currencies in 2010. So when the developed economies were reeling from a trade war with China and a subsequent global manufacturing recession threatened a full-on recession in 2019, the renminbi weakened along with other currencies.

This current episode is eerily similar. The dollar index has been gaining momentum along with the growth of the U.S. economy, even as the energy crisis threatens growth in the UK and Europe.

At the same time, the yuan has lost about 9% of its value versus the dollar as COVID-19 shutdowns threaten China’s economic growth. (The consensus forecast is for China’s real GDP growth to fall from 8.1% in 2021 to 3.5% this year, which is a virtual recession by China’s standards.)

The 12-month forward market is pricing in less than 1% appreciation of the yuan from current levels, hardly a sign of manipulation.

To argue that China should either widen its trading band or accept the shock absorber offered by a free-floating currency is probably secondary to the conversation over dealing with state control of energy supplies.

Let's Talk!

Call us at +1 213.873.1700, email us at solutions@vasquezcpa.com or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-09-14.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/the-reign-of-king-dollar-will-continue-amid-a-global-flight-to-safety/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Vasquez & Company LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Vasquez & Company LLP can assist you, please call +1 213.873.1700.

Subscribe to receive important updates from our Insights and Resources.